Table of Links

2. Financial Market Model and Worst-Case Optimization Problem

3. Solution to the Post-Crash Problem

4. Solution to the Pre-Crash Problem

5. A BSDE Characterization of Indifferences Strategies

Acknowledgments and References

Appendix A. Proofs from Section 3

Appendix B. Proofs of BASDE Results from Section 5

Appendix C. Proofs of (CIR) Results from Section 6

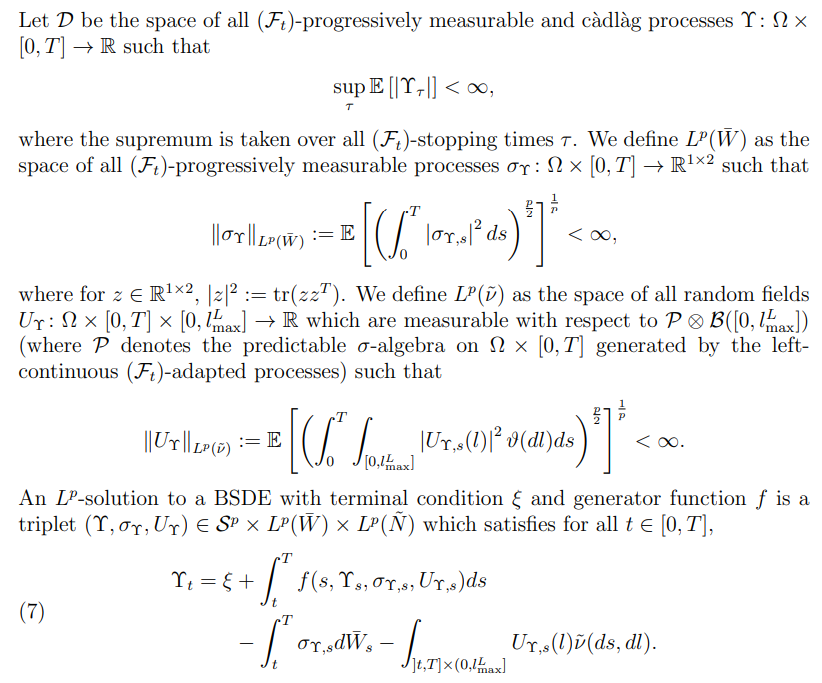

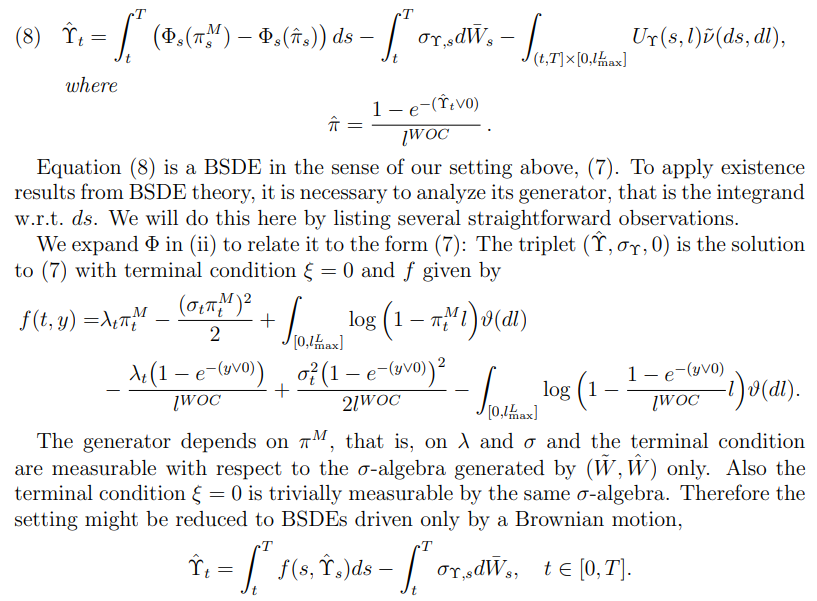

5. A BSDE Characterization of Indifference Strategies

In the previous section we have seen how (super-/sub-)indifference strategies can be useful to derive bounds for the worst-case optimal solution. In this section we discuss indifference strategies in more detail using a characterization in terms of backward stochastic differential equations (BSDEs). This is completely analogous to the ODE characterization of indifference strategies in the literature on worst-case optimization for constant market coefficients, cf. for instance [39, 34, 37]. In what follows we use the following notations for BSDEs: Let W¯ denote the vector of our independent driving Brownian motions

Specifications for the generator and the terminal conditions will be given further below.

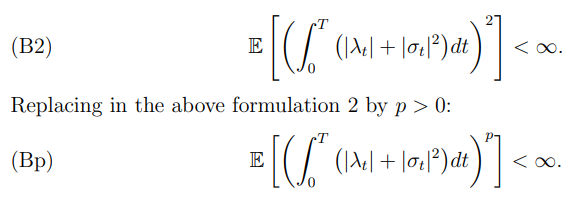

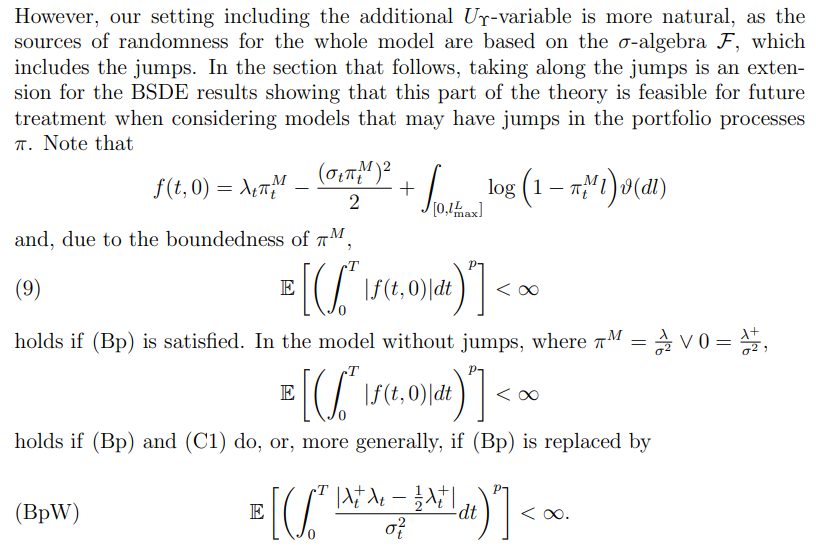

To be able to apply all the necessary BSDE machinery, we need to make for now stronger integrability and boundedness assumptions on the underlying market model. First, we consider a set of assumptions that strengthen the integrability assumption (B1):

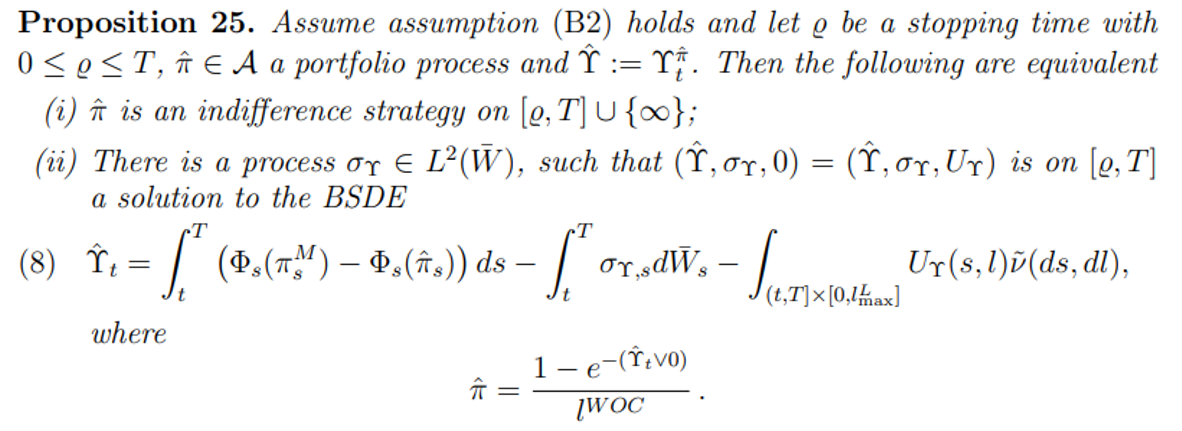

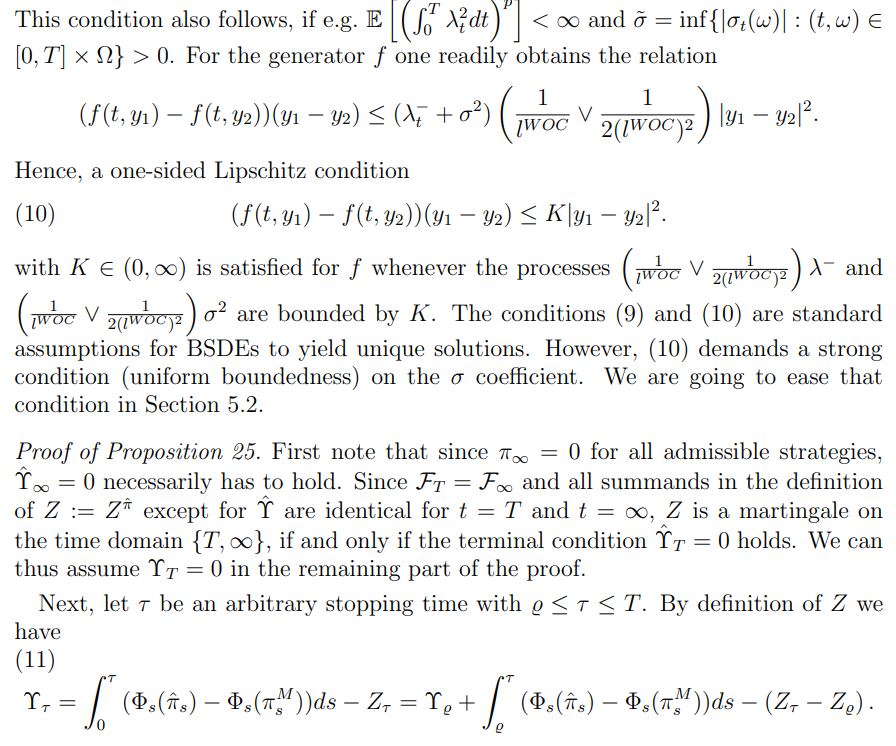

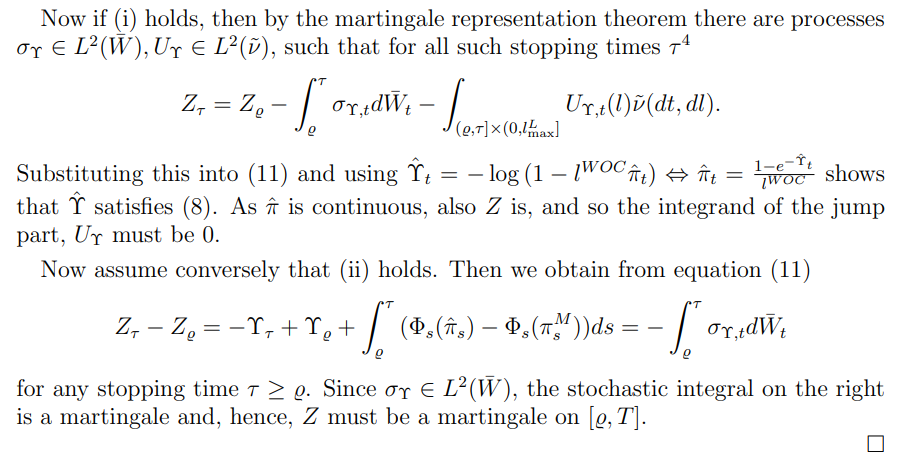

5.1. Analysis of the Generator. The following proposition provides the fundamental link between indifference strategies and BSDEs

With stronger tail properties, in addition to existence, the following theorem grants uniqueness of solutions in a class of functions.

5.3. Existence of Indifference Strategies. We now have everything at hands in order to prove the existence of a unique indifference strategy. In particular, combining Proposition 25 with ϱ = 0 and Theorem 30 implies the following uniqueness result.

On the one hand, for any particular model one thus needs to come up with additional arguments why this proposition is applicable. On the other hand, however, these results are useful in the important special case of a constant post-crash optimal strategy, that is, if assumption (C2) is satisfied. In this case we can conclude:

These existence results will also be of use in the following sections when dealing with concrete examples and numerical investigations.

:::info

Authors:

(1) Sascha Desmettre;

(2) Sebastian Merkel;

(3) Annalena Mickel;

(4) Alexander Steinicke.

:::

:::info

This paper is available on arxiv under CC BY 4.0 DEED license.

:::